Invest or Pay Off Debt? Discover Which Option is Best for You

September 8, 2023

5:19 am

If you’re paying off a loan (say a home or car loan) and suddenly find yourself with some extra cash, you might be wondering whether to put it towards paying off the loan or investing.

It’s a tricky choice, but we’ve got some insights to help you make the right decision.

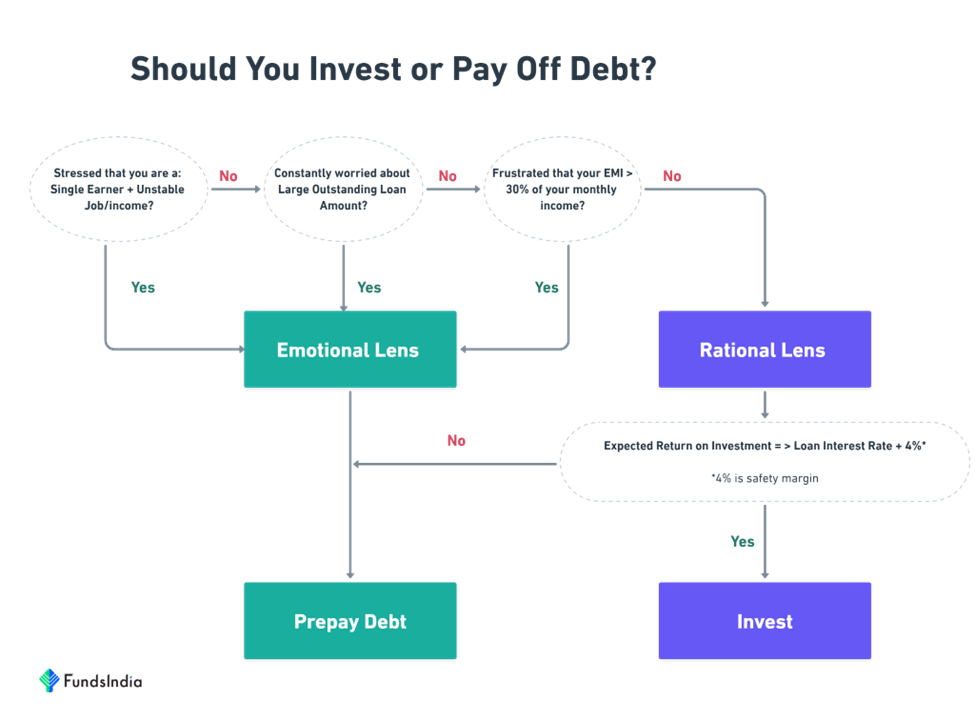

There are basically two lenses that you can use to solve the dilemma:

LENS 1: RATIONAL LENS

The logical starting point is to compare the expected future return from your investment vs your current loan’s interest rate.

Buffer for rising interest rates – In the last few months the loan interest rates have increased from 6% to almost 8-9%. To provide for such rising rates an additional buffer is required.

Buffer for unexpected Investment returns – There can be times when the Investment returns do not turn out as expected, for such lower than expected return outcomes a buffer is required.

Here is an example of how this works.

Assume you plan to invest in Equity Mutual Funds and your return expectation is around 12%.

Your current home loan rate is at 9%.

So,

Expected Return from Investment at 12% < 13% (i.e. Loan Interest Rate of 9% + Safety Margin of 4%)

This means from a rational point of view, it’s better to ‘Prepay Debt’

LENS 2: EMOTIONAL LENS

Sure, the rational perspective makes logical sense. But let’s be real, when it comes to making decisions, emotions can play a huge role too. In fact, sometimes our emotions are just as important as the rational side of things, if not more.

So, let us also wear the emotional lens and check how you feel about the outstanding loan and monthly EMIs?

Question 1: Are you stressed that you are a single earner and have an unstable job/income?

If yes, it is better to prepay debt.

Question 2: Do you constantly worry about your large outstanding loan amount?

If yes, it is better to prepay debt which helps reduce the stress and burden.

Question 3: Are you frustrated that your monthly EMIs take away a large part (>30%) of your monthly income?

If yes, it is better to prepay debt.

So, how do we know when to apply which lens?

The decision flowchart below will help understand when to use which lens.

Summing it up

There are two lenses to evaluate this dilemma of prepaying debt vs investing.

The Rational lens is where you compare the expected investment returns and the loan interest rate. The Emotional lens is where you make decisions based on how you feel.

While both lenses are equally important, you can use the above framework to prioritize.

Thank you for your sharing. I am worried that I lack creative ideas. It is your article that makes me full of hope. Thank you. But, I have a question, can you help me?

Thank you for your sharing. I am worried that I lack creative ideas. It is your article that makes me full of hope. Thank you. But, I have a question, can you help me?

House Hunting – The Art of Choosing Between Renting and Buying

September 6, 2023

1:27 pm

mint genie. Click here to read it

Imagine the excitement and happiness that comes from buying your first home. For most of us it’s a big step in life and a moment of pure pride.

But it’s also important to remind ourselves that this involves a huge commitment financially.

This means we need to think through our decision both from an emotional and rational perspective.

So, how do we decide if it’s better to buy or rent your home?

Here’s a simple framework for navigating this decision and striking the right balance between what you want and what makes sense.

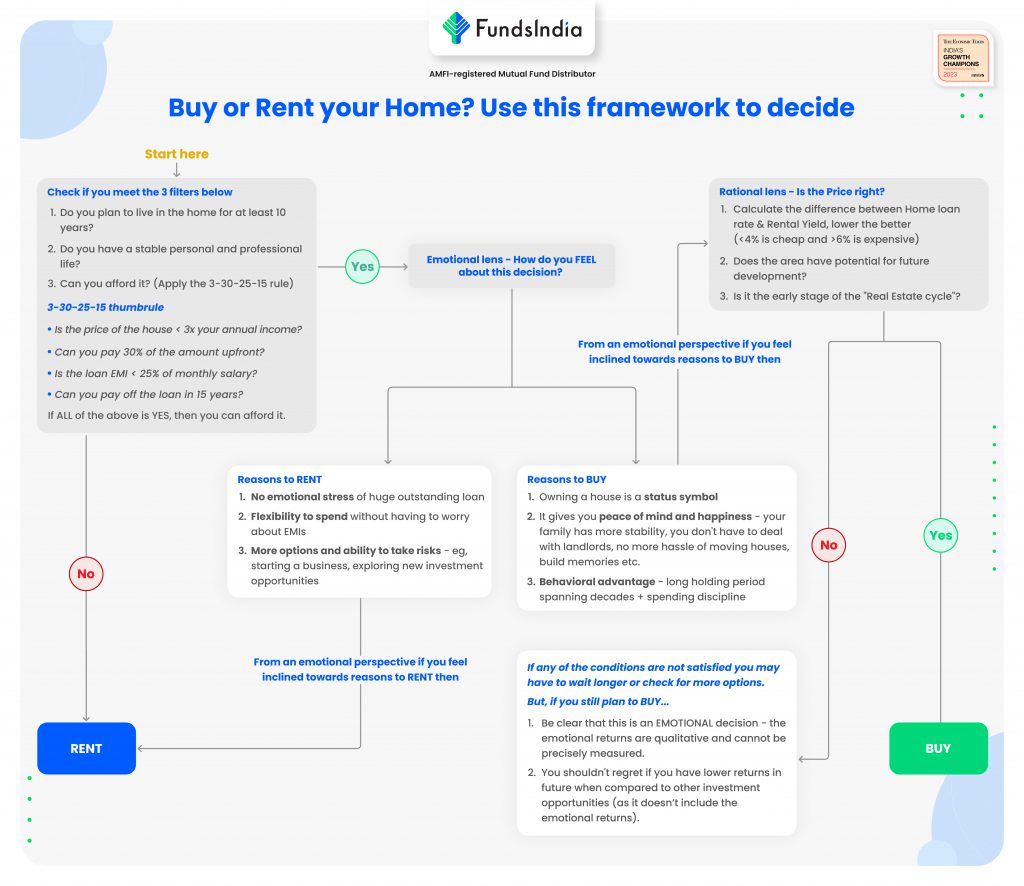

Step 1: The “3 Filter” Test

Filter 1: Do you plan to live in the home for at least 10 years?

If you have a profession which may require you to shift to another place or you want to explore other work opportunities which require you to move out of the current location then it is best for you to RENT your home.

Filter 2: Do you have a stable personal and professional life?

If you have an unstable job/profession or an unstable personal life then buying a home on loan will add to the stress. In this case it is best for you to RENT your home until there is stability.

Filter 3: Can you afford to buy this home?

Apply the 3-30-25-15 thumb rule to check your affordability:

Is the price of the house < 3x your annual income?

Can you pay 30% of the amount upfront?

Is the Loan EMI < 25% of your monthly salary?

Can you pay off the loan in 15 years?

If all the above is YES then it means you can afford to buy the home

Decision Point:

Did you pass the three filters?

No = RENT YOUR HOME

Yes = Move to the next Step

Step 2: Emotional Lens – How do you FEEL about this decision?

Emotional Reasons to RENT

No emotional stress of a huge outstanding home loan

You have the flexibility to spend well and do not have to worry about EMIs

You have more investment options and higher ability to take risks. Eg: starting your own business, exploring new investment opportunities etc.

Emotional Reasons to BUY

Owning a house is a status symbol and signals to others that you are successful

It gives you peace of mind and happiness – your family has more stability, you don’t have to deal with landlords, no more hassle of moving houses, you build memories etc.

Behavioral advantage – inculcates the habit of saving (EMIs), controls spending, and discipline to hold the asset for a long time (spanning decades).

Decision Point:

If you feel inclined towards reasons to rent = RENT YOUR HOME

If you feel inclined towards reasons to buy = Move on to the next Step

Step 3: Rational Lens – Is the Price Right?

Now your next step is to find out if the price of the house is right. These three vantage points will help you do that

Is it cheap or expensive?

In order to determine whether the price of the house is cheap or expensive, you can compare the Home Loan rate and the Rental yield.

Rental Yield is the Annual Rental Income (that you can get if you rent it out) as a Percentage of House Price.

Rental Yield = Annual Rent ➗ Price of the house

When it comes to rental yields, higher the better!

Now, calculate the difference between home loan rate and rental yield.

Lower the difference, the better.

Home loan rate – Rental yields < 4% = CHEAP

Home loan rate – Rental yields > 6% = EXPENSIVE

Here is an example of how this works,

Assume the price of the house is Rs 1 crore and the monthly rent is Rs 20,000 (so yearly it is Rs 2.4 lakhs) and your current home loan rate is 9% .

Rental yield = 2.4% (Rs 2.4 lakh ➗ Rs 1 crore)

Home loan rate 9% – Rental yield 2.4% = 6.6%

This means the price is expensive right now.

Is there potential for future development in your chosen area?

A property’s return potential is highly dependent on its location, neighborhood, amenities, connectivity, and future development prospects.

This includes

Current access to facilities like offices, schools, hospitals, malls and markets, and transportation hubs

Connectivity to major roads, highways, and public transportation etc.

Future developments like planned public or private infrastructure projects, metro rail, flyovers, schools, markets, hospitals etc

These factors will help you assess the scope for future development when purchasing real estate.

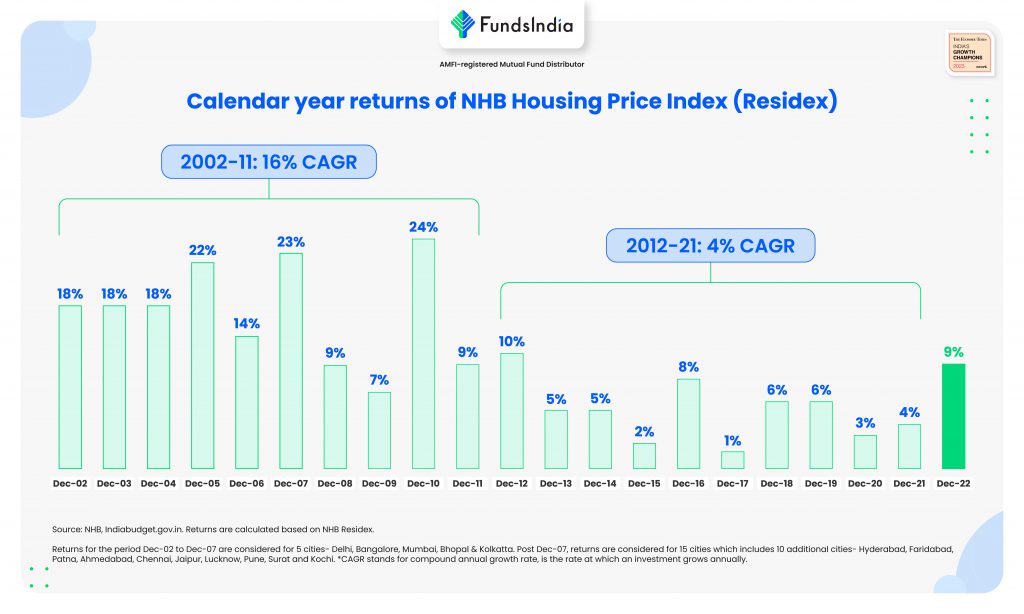

Where are you in the real estate cycle?

Understanding the real estate cycle is important to know if the price is right and what to expect as future appreciation. Real estate prices typically experience cycles characterized by a period of upward momentum lasting 7-10 years, followed by a subsequent downturn.

So, ‘WHEN’ you enter the real estate cycle is a key determinant of your long term returns.

In the chart below we can see the last 20 years returns from an investment in real estate,

2002-2011 – 16% annualized returns (up-cycle)

2012-2021 – 4% annualized returns (down-cycle)

As seen above, it is better to buy at the early stages of the real estate cycle

How do we know it is the early stages of the next up-cycle?

Here are some factors to identify this

Low Past Returns – if the prices have been stagnant (time correction) or declined over the last 7-10 years. Check for early signs of a price pick up.

Low Supply – Unsold inventory is reducing and there are few or no new real estate project announcements.

Low Home Loan rates – If home loan rates are low compared to the last 20 year history

Improving Demand – led by better affordability – higher salaries, lower interest rates and lower house prices

Together, these factors provide an indication of the early stage of an up-cycle.

In short, the price is right if

The difference between home loan rate and rental yields does not exceed 6% (>6% is expensive)

The area has potential for future development and price appreciation

You are investing at the early stage of the real estate cycle

If any of the above conditions are not met, then it means the price is not right.

So, what happens when the price is not right?

You will have to WAIT LONGER to buy the right property or look out for MORE OPTIONS with the RIGHT PRICE.

But, even when the price is not right and you still want to buy a house, what to do?

Remember this,

Be clear that this is now an EMOTIONAL decision – the emotional returns are qualitative and cannot be precisely measured.

You shouldn’t regret if you end up with lower returns in future when compared to other investment opportunities (as it doesn’t include the emotional returns).

Once you come to terms with the above two realities, you can go ahead and still buy the home though the price is not favorable

Summing it up… Visually!

An overview of this simple framework can be found in the visual flowchart below.

Demystifying Home Loan EMIs: What They Don’t Tell You

September 6, 2023

1:27 pm

financial express. Click here to read it

Do you have a home loan outstanding or are you planning to take a home loan?

If ‘Yes’, do you really understand the nuances of how a home loan EMI works?

Let’s find out.

Try and answer these 3 questions.

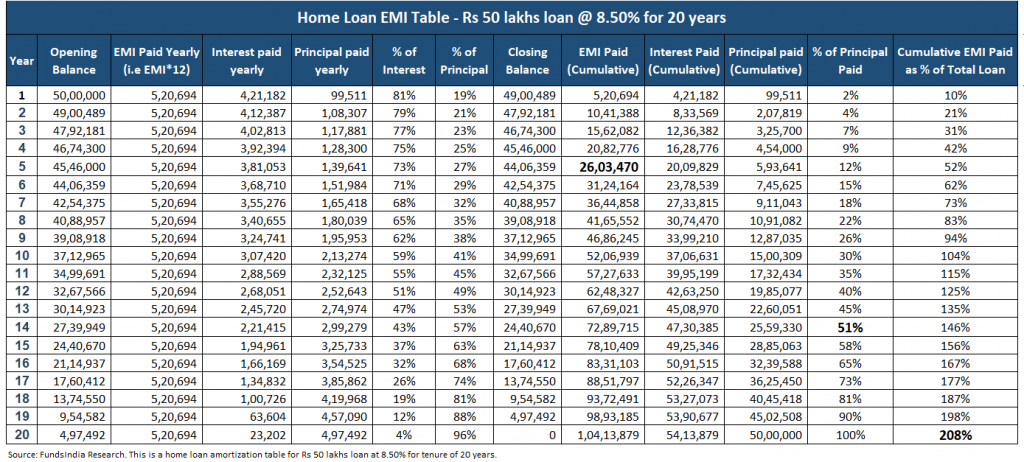

Assume you have taken a home loan of Rs 50 lakhs at 8.50% interest for a tenure of 20 years with an EMI of Rs 43,391.

Question 1: In the first 5 years you would have paid a total EMI of ~Rs 26 lakhs (read as more than 50% of your original loan amount). How much of your principal loan amount have you repaid?

Option A – 30% to 40%

Option B – 20% to 30%

Option C – less than 15%

Question 2: For the 20 year home loan, how long does it take to repay 50% of the loan amount (principal)?

Option A – 10 years

Option B – 12 years

Option C – 14 years

Question 3: For the loan of Rs 50 lakhs, what is the total EMI amount that you pay over 20 years?

Option A – Rs 70 lakhs to Rs 80 lakhs

Option B – Rs 80 lakhs to Rs 90 lakhs

Option C – more than Rs 1 cr

Now let’s check if you got them right!

The correct answers are,

Question 1: In the first 5 years you would have paid a total EMI of ~Rs 26 lakhs (read as more than 50% of your original loan amount). How much of your principal loan amount have you repaid?

Correct Answer – Option C (less than 15%) – its actually 12%!!

Question 2: For the 20 year home loan, how long does it take to repay 50% of the loan amount (principal)?

Correct Answer – Option C (14 to 15 years)

Question 3: For Rs 50 lakhs home loan, what is the total EMI amount that you pay over 20 years?

Correct Answer – Option C (more than 1 cr) – its 1.04 crs

Surprised!

Here is the evidence – the Detailed Home Loan EMI table which shows the 20 year journey

*You can refer to the annexure section of the blog to understand the various columns

How does a home loan really work: 3 Surprising Insights!

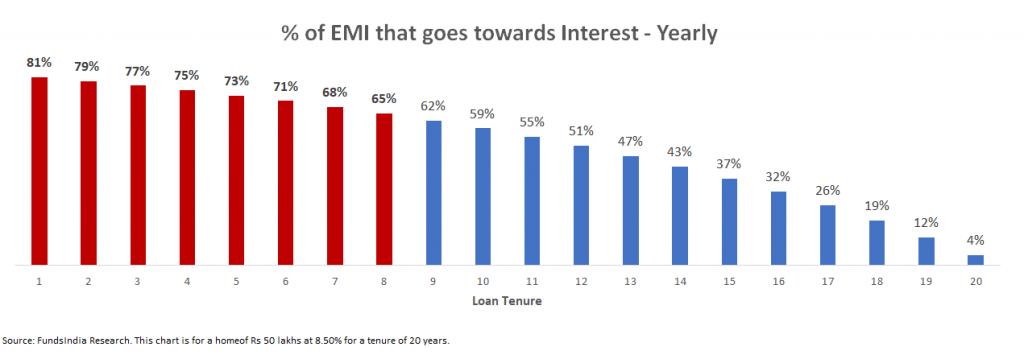

INSIGHT 1: During the initial years, most of your EMI goes only for interest payments!

Sample this.

For a Rs 50 lakhs home loan for 20 years at 8.5% interest rate…

In the first year, out of Rs 5.20 lakhs that you paid as EMI, Rs 4.2 lakhs goes only towards Interest – a massive 81% of your yearly EMI!.

5 years later, the total cumulative EMI amount is Rs 26 lakh, out of which Rs 20 lakhs (77% of cumulative EMI) were only interest payments!

Why does this happen?

As seen from the chart below, a large percentage of your EMI in the initial years goes only towards Interest.

Does this hold true for different loan rates?

Yes it does. Historically, in India interest rates have been around 7% to 9%.

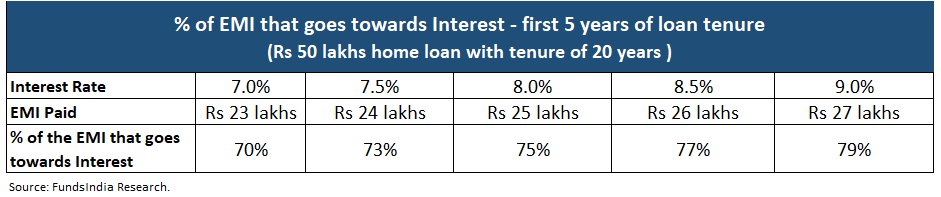

Assuming 7-9% home loan rates, around 70%-80% of the EMI that you pay in the first 5 years goes only towards Interest!

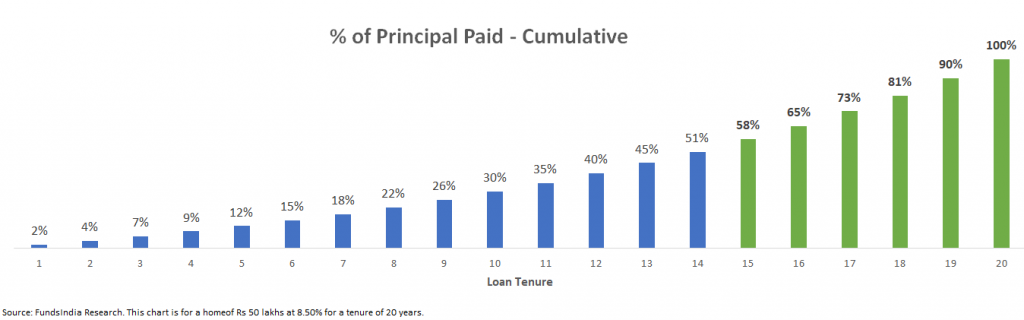

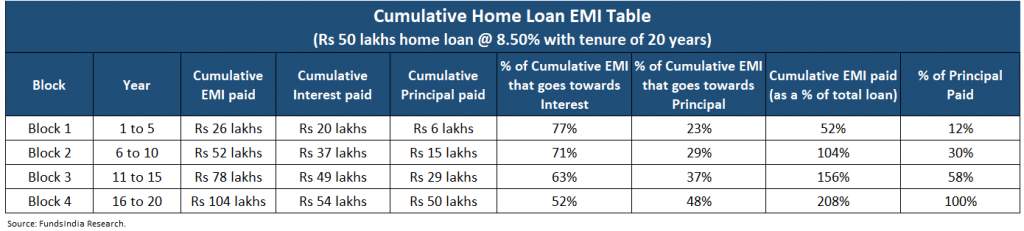

INSIGHT 2: While you pay off almost HALF of the loan amount as EMIs in the first five years, only 10-15% of the loan is paid off!

During the initial years of the loan tenure the contribution of EMI towards the Principal is low which means the loan amount (principal) repaid is also low.

In the chart below, for the same example of a Rs 50 lakhs home loan for 20 years at 8.5% interest rate, you can see how much of the original loan gets repaid cumulatively after every year.

Here comes the shocker…

In the first 5 years the principal repaid is only 12% despite paying off 50% of the home loan as EMIs!

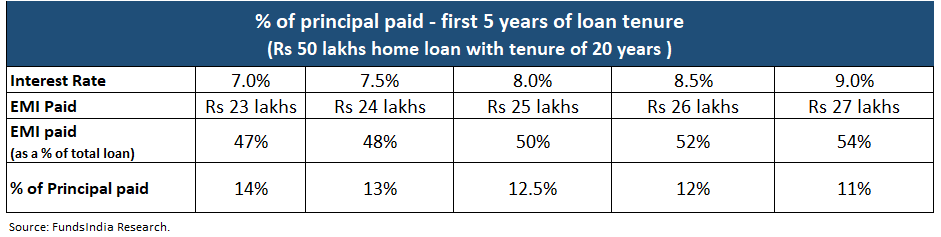

Let’s check if this holds true for different interest rates (7% to 9%).

As seen above, this holds true across different home loan rates between 7%-9%.

Only 10-15% of the loan gets paid off the first 5 years despite paying off almost half the loan amount (45%-55%) as EMIs.

INSIGHT 3: You almost end up paying TWICE the original loan amount as EMIs for a 20-year home loan

While we regularly track the EMIs, Interest and Principal, what we usually overlook is the total amount that we have to pay for the home loan over the entire tenure.

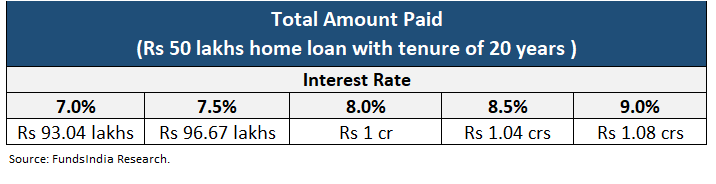

For a Rs 50 lakhs home loan at 8.5% interest, you end up paying Rs 1.04 cr over 20 years – this is almost 2 times the loan amount!

Interest is more than the loan amount i.e. Rs 54 lakhs!

In the table below you can see that even at different home loan rates (7-9%), you still end up paying almost 2 times the original loan amount.

Understanding all the above 3 nuances of how a home loan really works, is important to ensure that you don’t get frustrated in the initial years.

3 Ideas to manage your home loan better

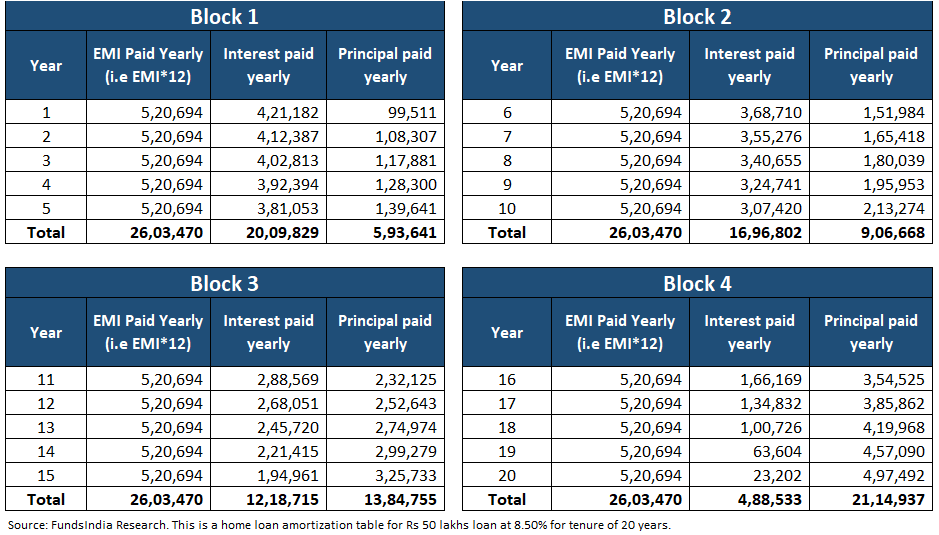

IDEA 1: Use 5 year cumulative blocks to understand how your home loan EMI is split across Interest and Principal

Assume you have a loan tenure of 20 years. To make it simpler, divide this into 5 year blocks (4 in this case) and summarize the cumulative totals.

This makes it easier and simple to understand the proportion of EMI that goes towards Principal vs Interest.

To calculate this, you can use the home loan EMI calculator here.

IDEA 2: Try to prepay in early years and increase your EMI every year in line with your salary increase

Since in the early years of loan tenure the majority of EMI goes towards interest, it is better to prepay some of your home loan in the initial years of the loan tenure which will help reduce the total amount paid (over the tenure for the loan) and shorten the loan tenure. Home loan prepayments simply mean you pay a certain portion of your loan amount earlier than the planned repayment period.

This can be done in two ways

Increasing your EMI every year as your salary increases

Prepay whenever you receive any lumpsum amount or bonus

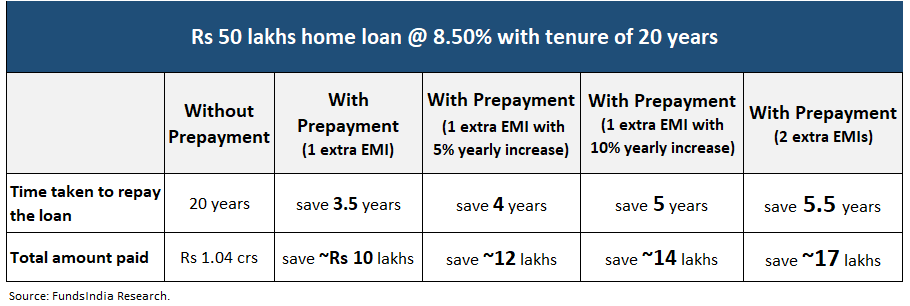

How much of a difference does it really make?

If you prepay 1 extra EMI every year, then your total EMI payments (over the loan tenure) reduce by almost 20% of the original loan amount.

If you prepay 1 extra EMI and also increase this by 5% every year, then your total EMI payments reduce by almost 25% of the original loan amount.

This gets even better if you are able to prepay more/increase the EMI.

In the table below we have compared the Rs 50 lakhs home loan assuming no prepayment, with prepayment and with yearly increase in prepayment.

IDEA 3: If home loan rates go up, don’t forget to increase EMI or Prepay to keep tenure constant

While taking a home loan we usually keep the prevailing home loan rate in mind and do not plan for situations like an increase in home loan rates. When interest rates go up, while your EMI remains the same, the banks increase the tenure of your loan.

So, whenever your home loan rates increase, don’t forget to increase your EMI or prepay – to keep your loan tenure the same.

Summing it up

Understand these 3 nuances of a home loan EMI

During the initial years, most of your EMI goes only for interest payments

While you pay off almost HALF of the loan amount as EMIs in the first five years, only 10-15% of the loan is paid off

You almost end up paying TWICE the original loan amount as EMIs for a 20-year home loan

Use these 3 ideas to manage your home loan better

Use 5 year cumulative blocks to simplify and understand how your home loan EMI is split across Interest and Principal

Try to prepay in early years and increase your EMI every year in line with your salary increase

If home loan rates go up, don’t forget to increase EMI or Prepay to keep tenure constant

Annexure:

Home Loan EMI table Glossary:

Opening Balance = loan outstanding at the start of the year

Thank you for your sharing. I am worried that I lack creative ideas. It is your article that makes me full of hope. Thank you. But, I have a question, can you help me?

3 thoughts on “Invest or Pay Off Debt? Discover Which Option is Best for You”

Thank you for your sharing. I am worried that I lack creative ideas. It is your article that makes me full of hope. Thank you. But, I have a question, can you help me?

Thank you for your sharing. I am worried that I lack creative ideas. It is your article that makes me full of hope. Thank you. But, I have a question, can you help me?

Your article helped me a lot, is there any more related content? Thanks!